Earnings Power Value (EPV) also known as just Earnings Power is a valuation technique popularized by Bruce Greenwald, an authority on value investing at Columbia University. It is arguably a better way to analyze stocks than Discounted Cash Flow analysis that relies on highly speculative growth assumptions many years into the future.

EPV uses a very basic equation which assumes no growth, although it does rely on an assumption about the cost of capital as well as the fact that current earnings are sustainable. It also involves several adjustments to clean up the underlying Earnings figures.

How does EPV work?

EPV is a technique for valuing stocks by making an assumption about the sustainability of current earnings and the cost of capital but assuming no further growth.

EPV = Adjusted Earnings / Cost of Capital

While the formula is simple, finding the adjusted earnings can be tricky and must consider operating profit, taxation adjustments and depreciation.

Now lets us look at EPV for GADANG.

The EPV equation is Adjusted Earnings divided by the company’s Cost of Capital. This is calculated in 6 simple steps as follows:

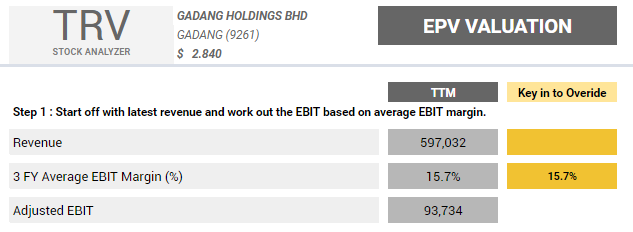

Step 1 : Start off with latest revenue and work out the EBIT based on average EBIT margin.

The starting point is revenue. We then work out the average EBIT (Operating margin) to arrive at the adjusted EBIT number.

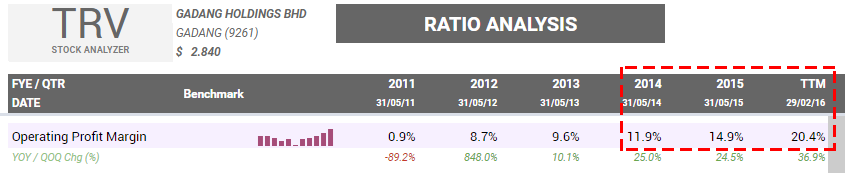

Click to enlarge. Diagram showing Operating Profit Margin for Gadang.

Click to enlarge. Diagram showing Operating Profit Margin for Gadang.

Notice that Gadang’s operating profit margin has been rising. We take the average of last 2 years and TTM operating margin. The average operating profit margin come out to be 15.7%.

Click to enlarge. Diagram showing Step 1 for Gadang EPV.

Step 2 : Apply the average tax rate to the adjusted EBIT

To the above figure, we apply a normalised tax rate – this could either be the average tax rate of the company over, say, the last 5 years or alternatively use the general corporate tax rate to avoid the distortive effect of different tax schemes

Step 3 : Add D&A and deduct maintenance CAPEX.

This is Economic Depreciation Adjustment. This involves adding back the depreciation figure of the average most recent year and deducting the maintenance capital expenditure. Maintenance CAPEX is calculated by take the average CAPEX over the period of 10 years.

Click to enlarge. Diagram showing Step 2 & 3 for Gadang EPV.

Step 4 : Divide by the discount rate

From the normalized income, we then divide with the discount rate. For this valuation, we will use the discount rate of 10%.

Step 5 : Add cash & Deduct debt and minority interest

It is then necessary to subtract out any corporate debt and add in cash in excess of operating requirements to come to the EPV of the firm.

Step 6 : Divide by number of shares

To compare this to the share price, EPV value is divided by the number of shares.

Click to enlarge. Diagram showing Step 4, 5 & 6 for Gadang EPV.

The EPV for GADANG is at RM3.25 pershare. From the current price of RM2.84. It still offer a margin of safety (MOS) of 12.7%.

I have previously written two articles on DCF valuation and Benjamin Graham’s Formula valuation for GADANG.

Let’s look at the average of Gadang’s valuation based on all 3 methods.

EPV Valuation – RM 3.253

Ben. Graham Formula – RM 3.364

Average Valuation = RM 3.255

Summary on EPV

The great advantage of this technique as it does not muddy the valuation process with future predictions. It evaluates a company based on its current situation. That is also however also potentially a weakness in that it may systematically undervalue growth companies. Value investors might regard this as being part of the margin of safety but in normal markets, it may even be difficult to find a company that’s selling for less than its EPV.

Another potential weakness is its reliance on earnings, given the scope for companies to manipulate/massage this figure.

Leave A Comment